Happy new year everyone! 2014 is here, with new opportunities and new challenges.

We are entering into the new year with a booming economy in the Unites States and Japan, with Europe slowly reemerging from recession, and China tagging along its new trend growth (e.g. around 7% p.a.).

The picture is mixed in other BRICs countries, with India experiencing slower growth as a result of bad government policies, and Brazil suffering from higher US interest rates. Though higher, interest rates are still record low in a historic context, making no doubts about the role of credit financed investment once again becoming the key driver of growth.

Before making bold predictions about future investment opportunities, it makes sense to reconcile past predictions. There is no better place to start than with past expectations that resulted in money being placed, underlining the conviction behind the predictions made. Hence, I start the first blog of the new year with a review of the Model Portfolio.

The Model Portfolio is up 62% since November 2012. As it was initiated only a bit more than a year ago, annualized returns to date are 51%.

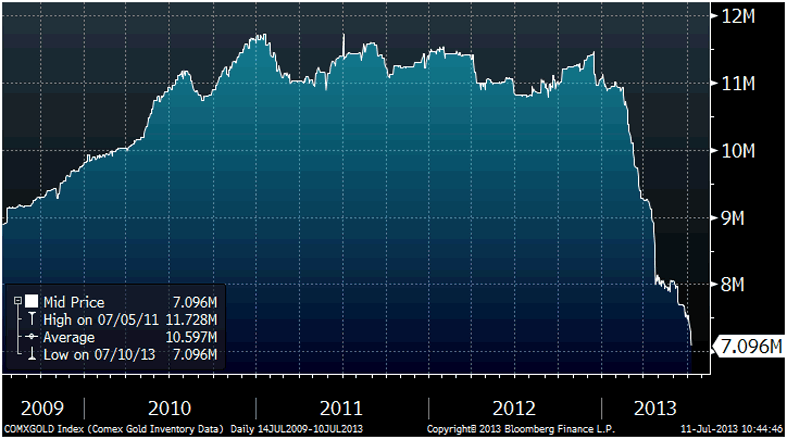

Portfolio assets were selected with the objective to minimize the risk of overall market fluctuations ("systemic risk") and only take specific positions in assets with opposite reactions to the same underlying macroeconomic driver (e.g. negative correlation). In order words, the portfolio was designed to do well independently of whether the overall stock market went up or down. A long position is Google was balanced against a short position in Apple. And a long position in Bank of America was partially off-set with a long position in gold (US recovery is positive for BAC, but negative for gold).

Common to all positions was a belief in increased liquidity in financial markets, eventually driving global inflation. As the first step in an inflationary cycle is asset inflation, the expectation has been met by surging asset values in nearly all global markets, across nearly all asset classes (commodities still being the general exception).

In spite of massive monetary stimuli by all major global central banks, inflation has still not reached Consumer Price Indexes, and has therefore still not reached the point of distorting prices, thus leading to economic inefficiencies.

Several reasons have been offered for why this has not happened yet. Behavioural economist have been pointing out that the debt loving baby boomer generation has been retiring in the US, with younger generations having a more prudent view on debt financed spending. Others have pointed out that the credit worthiness of millions of Americans has been impaired during the financial crisis, thus making them less able to borrow.

I think the explanation is much much simpler than that. In my view, there is one factor alone that overwhelmingly explains why inflation today is not double digit: The capital reserve requirement for banks has increased dramatically in the aftermath of the financial crisis.

In 2008, average banking Tier 1 capital requirements were only about 4-5% of total assets. As this implied banks could lend 20 dollars for each dollar of reserves, every new dollar created by the central bank implied 20 new dollars in circulation. Today, average banking Tier 1 reserve ratios are above 15%. That means every new dollar created is only equivalent to less than 7 new dollars in circulation.

If banks had gone from 5% to 15% capital reserve requirements without the central bank increasing the money supply, simple math suggests the affected economies would have experienced a deflation of nearly 70% (equivalent to the reduction in credit and money in circulation). Interestingly, the increase in the monetary base has been very near this figure. So central banks have been able to pull through the miracle of financing increased government spending with new money without causing inflation.

A second relevant, more intermediate factor, is that since price increases are caused by more money in circulation chasing the same amount of resources, inflation will not materialize as long as there is surplus supply of a resource at the given price level.

In the market for labour, this is illustrated by the Phillips Curve (see a previous post), which simply states that inflation will not materialize as long as unemployment is above a certain level. Philips called this the "equilibrium unemployment rate". Below this level, for the US recently estimated to be around 6%, competition for labour will push up wages, creating more demand from consumers, driving up general prices.

Hence, for inflation to materialize, the global economy must first face an economic boom, were unemployment first reaches record lows. Then wages will increase. Unless interest rates then rise to slow the economy down, wage increases will continue to drive increased demand, re-inforcing the boom, eventually causing commodity prices to increase, causing inflation to escalate.

Since the debt levels today are still very high in the economy, the central bank is likely not to raise interest rates before inflation has run its course for several years. If too high inflation goes on for too long, it will cause allocation of resources to unproductive sectors of the economy, making the recession extremely painful once the central bank eventually decides to apply the brakes (like Paul Volcker did in 1981). An extreme case of a recession following a period of high inflation also happened in Germany in the 1930s, eventually creating a political sentiment supportive of Adolf Hitler coming to power.

OK, now this post is becoming much longer than I had intended. So let me get to what the expectations are for the Model Portfolio.

I am convinced that we are now in the very early phases of what will eventually become an inflationary boom. The reasons for this is that capital requirements of banks are unlikely to increase further, so the sterilizing impact this has had on money in circulation is unlikely to continue. Meanwhile, the FEB, ECB, BoJ, Bank of China, all of them have continued issuing new money at almost the same speed.

This should continue to lift the Model Portfolio higher, with the exception that gold will only start moving AFTER the other positions have flattened out their surge.

With unemployment in the US currently at 6.7%, it is likely to reach below 6% sometime during the second quarter of 2014. Inflation should materialize in paralell around that time, but will not escalate to problematic levels until unemployment goes down to around 5%.

When that happens (most likely in q3 or q4 of 2014), gold will be back in play. Meanwhile, there will be investment opportunities in markets that are still undergoing asset deflation (e.g. Spain, Greece, Italy). Stabilization of these economies imply they will be de-risked, and wage levels once again will become competitive, as the rest of the world will experience inflation.

Happy investing 2014!